pika: A lightweight package for evaluating correlation between time series

Kylie Ainslie

2026-01-05

Source:vignettes/pika_vignette.Rmd

pika_vignette.RmdOverview

pika is a lightweight package that enables easily

estimating the optimal lag and rolling corrleation between two time

series. This package was dveloped for use with epidemiological data and

mobility data, but can be used more generally for other time series. The

main utility of this package is the ability to determine quantities of

interest by a grouping variable, such as the rolling correlation between

two time series for different locations. This vignette goes over the

different functionality of pika in an epidemiological

context, namely determining the optimal lag and rolling correlation

between estimates of reproduction number (the average number of new

cases generated by a single case) and mobility within the population

within different regions of China during the COVID-19 pandemic.

Data

pika contains several example data sets in the

data/ directory that can be used to run through the package

functions. The example data sets include 1. Daily confirmed cases of

COVID-19 from different provinces in China (china_case_data) 2. Daily

within-city movement data for the same provinces in 1

(exante_movement_data)

The case data has daily confirmed confirmed cases for different provinces in China from 16 January to 24 March 2020 from the dashboard maintained by Chinese Center for Disease Prevention and Control (CCDC) [1]. The CCDC dashboard collates numbers of confirmed cases reported by national and local health commissions in each province in mainland China, and Hong Kong SAR and Macau SAR. Confirmed cases are defined as suspected cases, who have epidemiological links and/or clinical symptoms, and are detected with SARS-CoV-2 by PCR tests. However, in Hubei province, clinically diagnosed cases were additionally included between 12 and 19 February.

The daily within-city movement data, used as a proxy for economic activity, is available from 1 January to 24 March 2020 for major metropolitan cities within each province in mainland China, Hong Kong SAR, and Macau SAR. These data, provided by Exante Data Inc [2], measured travel activity relative to the 2019 average (excluding Lunar New Year). The underlying data are based on near real-time people movement statistics from Baidu.

Estimate effective reproduction number

To estimate the effective reproduction number (Rt), pika has a

function estimate_rt() that provides a wrapper for

EpiEstim::estimate_R() [3]

that enables users to estimate Rt by a grouping variable. As input

estimate_rt() takes a data frame of daily cases or deaths

by group. pika includes an example data set

china_case_data.rda that includes daily reported cases of

COVID-19 from several provinces in China between 16 January 2020 and 24

March 2020.

| date | province | cases |

|---|---|---|

| 2020-01-16 | Hubei | 4 |

| 2020-01-16 | Guangdong | 0 |

| 2020-01-16 | Zhejiang | 0 |

| 2020-01-16 | Henan | 0 |

| 2020-01-16 | Hunan | 0 |

| 2020-01-16 | Beijing | 0 |

| 2020-01-16 | Hong_Kong_SAR | 0 |

| 2020-01-17 | Hubei | 17 |

| 2020-01-17 | Guangdong | 0 |

| 2020-01-17 | Zhejiang | 0 |

To estimate Rt from case data, the user must specify the data set in

the dat = argument of estimate_rt(). The data

set should include three columns: a date column (this should be of class

‘date’), a grouping variable, and the value used to estimate Rt (most

commonly this is cases, but other quantities can be used, such as

deaths). The names of the columns in the input data set should be

specified as character strings in the grp_var =,

date_var =, and incidence_var = arguments.

# to estimate them with pika, use estimate_rt() ------------------------------------------

rt_estimates <- estimate_rt(dat = china_case_data,

grp_var = "province",

date_var = "date",

incidence_var = "cases"

) %>%

# a little data formatting--------------------------------------------------------------

mutate(province = to_snake_case(province)) %>%

select(-date_start) %>%

rename("date" = "date_end")| date | province | r_mean | r_q2.5 | r_q97.5 | r_median |

|---|---|---|---|---|---|

| 2020-01-23 | hubei | 5.158792 | 4.718609 | 5.618324 | 5.155387 |

| 2020-01-24 | hubei | 4.572393 | 4.232182 | 4.925570 | 4.570112 |

| 2020-01-25 | hubei | 4.561455 | 4.273269 | 4.858912 | 4.559824 |

| 2020-01-26 | hubei | 4.409607 | 4.166198 | 4.659828 | 4.408408 |

| 2020-01-27 | hubei | 6.501828 | 6.246638 | 6.762055 | 6.500942 |

| 2020-01-28 | hubei | 6.117626 | 5.906827 | 6.332068 | 6.116984 |

| 2020-01-29 | hubei | 5.421957 | 5.258101 | 5.588293 | 5.421521 |

| 2020-01-30 | hubei | 4.719259 | 4.592553 | 4.847667 | 4.718960 |

| 2020-01-31 | hubei | 4.086316 | 3.987002 | 4.186835 | 4.086104 |

| 2020-02-01 | hubei | 3.743788 | 3.662311 | 3.826149 | 3.743632 |

The method used to estimate Rt can be changed using the

est_method = argument. This argument takes the following

options:

c("non_parametric_si","parametric_si","uncertain_si","si_from_data","si_from_sample").

For methods that require specifying the mean and standard deviation of

the serial interval, these parameters can be set using the

si_mean = and si_std = function arguments. The

default values are si_mean = 6.48 and

si_std = 3.83 [4].

For more information on the methodology underlying

EpiEstim::estimate_R look at this vignette

or at help("estimate_R").

Lag

When determining the relationship between two time series it is

sometimes of interest to determine the lag at which the correlation

between the two time series is highest, we’ll call this the optimal lag.

To determine the optimal lag, the two time series must first be merged

into a single data frame. We do this below using dplyr’s

left_join() by date and

province.

# Join data sets together by date and province to determine cross correlation -----------

# for this we are using input rt estimates, not those estimated using pika::estimate_rt()

data_joined <- left_join(rt_estimates,

exante_movement_data,

by = c("date","province")

)| date | province | r_mean | r_q2.5 | r_q97.5 | r_median | movement |

|---|---|---|---|---|---|---|

| 2020-01-23 | hubei | 5.158792 | 4.718609 | 5.618324 | 5.155387 | 4.792658 |

| 2020-01-24 | hubei | 4.572393 | 4.232182 | 4.925570 | 4.570112 | 3.774731 |

| 2020-01-25 | hubei | 4.561455 | 4.273269 | 4.858912 | 4.559824 | 2.573851 |

| 2020-01-26 | hubei | 4.409607 | 4.166198 | 4.659828 | 4.408408 | 2.020488 |

| 2020-01-27 | hubei | 6.501828 | 6.246638 | 6.762055 | 6.500942 | 1.876848 |

| 2020-01-28 | hubei | 6.117626 | 5.906827 | 6.332068 | 6.116984 | 1.817556 |

| 2020-01-29 | hubei | 5.421957 | 5.258101 | 5.588293 | 5.421521 | 1.766298 |

| 2020-01-30 | hubei | 4.719259 | 4.592553 | 4.847667 | 4.718960 | 1.662975 |

| 2020-01-31 | hubei | 4.086316 | 3.987002 | 4.186835 | 4.086104 | 1.603111 |

| 2020-02-01 | hubei | 3.743788 | 3.662311 | 3.826149 | 3.743632 | 1.546469 |

We can then identify the optimal lag by calculating the cross

correlation between the two time series by the grouping variable at

different lags using the cross_corr function. The argument

max_lag = specifies the maximum lag to test. In the below

example it is set to 10 days. The subset_date = argument

allows the user to determine the cross correlation between the two time

series for a subset of the time window.

# # Determine lag with max cross correlation between Rt and movement ----------------------

lags <- cross_corr(dat = data_joined,

date_var = "date",

grp_var = "province",

x_var = "r_mean",

y_var = "movement",

max_lag = 10,

subset_date = "2020-02-15"

)

# use min lag across groups -------------------------------------------------------------

my_lag <- min(lags$lag)Once the optimal lag is determined, we must back date our Rt estimates without impacting the date of the movement variable.

# create lag date using max lag from cross_corr() ---------------------------------------

data_joined_lag <- rt_estimates %>%

mutate(date = date + my_lag) %>%

left_join(., exante_movement_data, by = c("date", "province"))Percent change relative to baseline

Sometimes, it is of interest to convert a count variable over time

into a percent change based on the average value in a specified baseline

period. Using calc_percent_change() users can specify a

baseline period that will them be used to determine the percent change

in their count variable time series. This function was written for

application to mobility data, where the percent change in mobility over

time relative to baseline is of interest. However, this function can be

applied to any count type time series.

perc_change_data <- calc_percent_change(dat = exante_movement_data,

date_var = "date",

grp_var = "province",

count_var = "movement",

n_baseline_periods = 7)| date | province | movement | perc_change |

|---|---|---|---|

| 2020-01-01 | anhui | 5.131897 | 0.9674739 |

| 2020-01-02 | anhui | 5.585968 | 1.0530762 |

| 2020-01-03 | anhui | 5.675878 | 1.0700261 |

| 2020-01-04 | anhui | 5.191629 | 0.9787347 |

| 2020-01-05 | anhui | 4.821942 | 0.9090406 |

| 2020-01-06 | anhui | 5.421992 | 1.0221631 |

| 2020-01-07 | anhui | 5.301700 | 0.9994855 |

| 2020-01-08 | anhui | 5.636145 | 1.0625356 |

| 2020-01-09 | anhui | 5.463023 | 1.0298983 |

| 2020-01-10 | anhui | 5.633986 | 1.0621285 |

Rolling correlation

It is often of interest to determine the relationship between two

time series, specifically the rolling correlation. The

rolling_corr() function calculates the rolling correlation

between two times series (x_var and y_var)

over a specified time window n =. Here, we calculate the

biweekly rolling correlation between Rt and movement. Since our data is

daily estimates of Rt and movement, we set n = 14. If our

data was monthly and we wanted to determine a 6 month rolling

correlation, we would set n = 6. The output of

rolling_corr() is a data frame with an additional column

added to the input dataset called “rolling_corr”. Depending on the value

of n, the first n values of “rolling_corr” are

NA.

# Determine rolling correlation between Rt and movement ---------------------------------

data_corr <- rolling_corr(dat = data_joined_lag,

date_var = "date",

grp_var = "province",

x_var = "r_mean",

y_var = "movement",

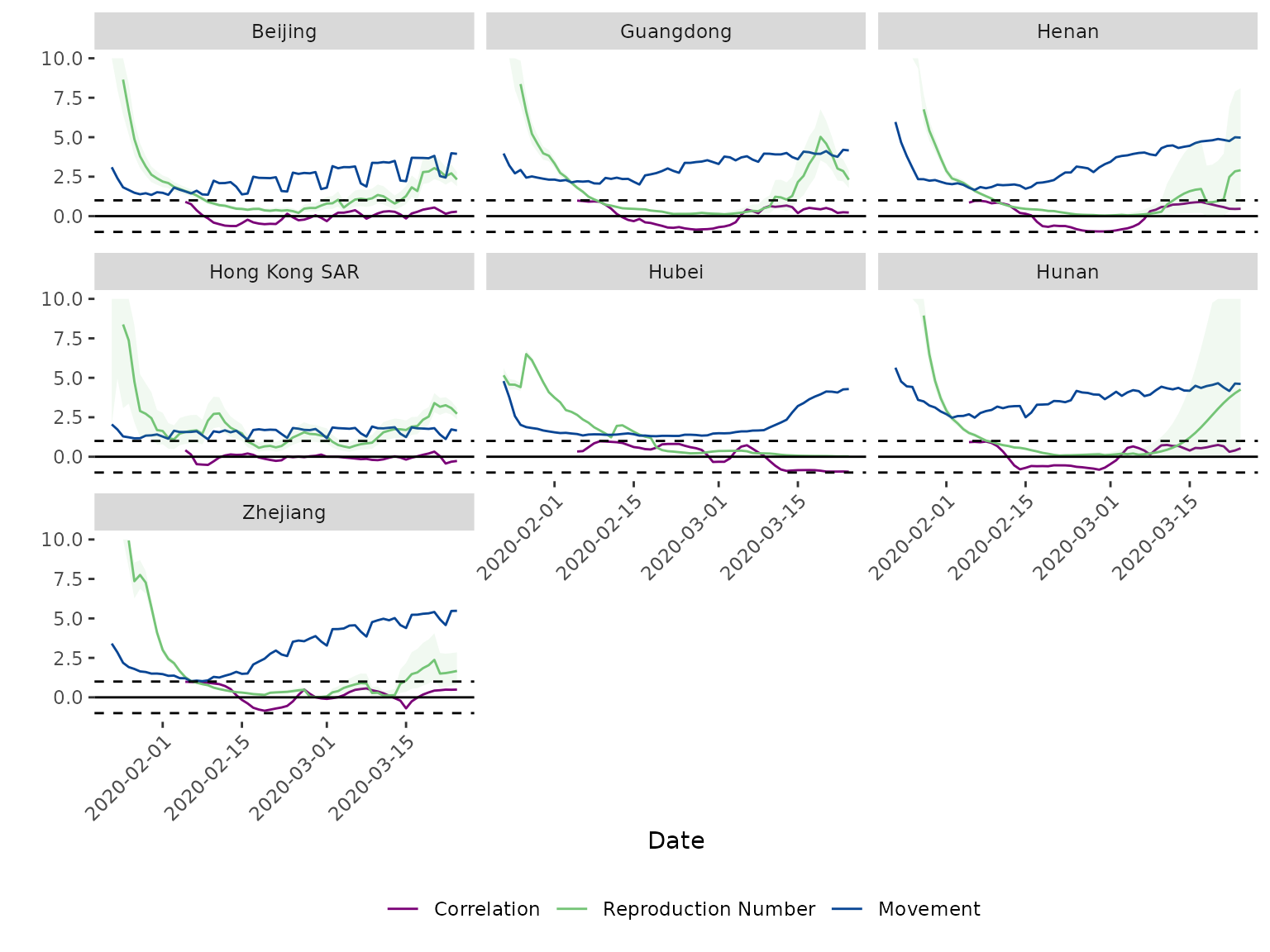

n = 14)To visualise the rolling correlation, the results of

rolling_corr() can be plotted using

plot_corr(). This creates a plot of the two time series and

the rolling correlation between them facetted by grouping variable.

There are optional arguments to change the facet labels

(facet_lables =), legend_labels

(legend_labels =), add confidence bounds for the primary

time series (x_var_lower = and x_var_upper =),

and set a maximum value for the y-axis (y_max =). The below

code plots the mean Rt estimates with 95% confidence bands, movement

index, and the biweekly correlation between them. We also specify custom

facet and legend labels and restrict the y-axis to a maximum value of

10.

# Plot Rt, movement, and correlation ----------------------------------------------------

my_labels <- c("beijing" = "Beijing", "guangdong" = "Guangdong", "henan" = "Henan",

"hong_kong_sar" = "Hong Kong SAR", "hubei" = "Hubei", "hunan" = "Hunan",

"zhejiang" = "Zhejiang")

my_legend = c("Correlation", "Reproduction Number", "Movement")

plot_corr(dat = data_corr,

date_var = "date",

grp_var = "province",

x_var = "r_mean",

y_var = "movement",

x_var_lower = "r_q2.5",

x_var_upper = "r_q97.5",

facet_labels = my_labels,

legend_labels = my_legend,

y_max = 10

)